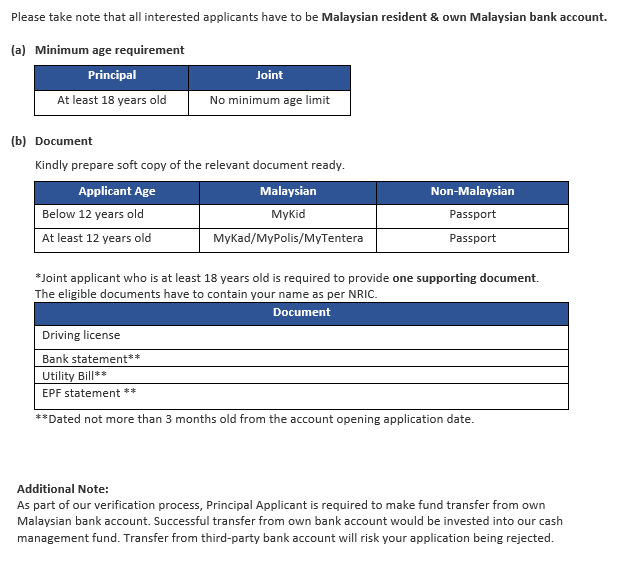

General Requirement to Open an Account

Investing into unit trust investments via i-Akaun/ i-Acccount

Frequently Asked Questions (FAQs)Members Investment Scheme (MIS) is an initiative by the EPF to provide investment options to members in enhancing their retirement savings. It allows only eligible members to voluntarily transfer a portion of their excess savings from EPF Account 1 to Fund Management Institutions (FMI)s for eligible investments. The MIS was introduced in November 1996.

You can invest through MIS if:

You can now invest through MIS using: (a) agents; or (b) the i-Akaun (Member). The Investment tab on the i-Akaun (Member) is an online, self-service function that does not require agents. As such, you may be charged higher fees when investing through agents versus the i-Akaun (Member).

Eligible investments under MIS are:

The EPF only approves unit trust funds that have a Simple Average Consistent Returns (SACR) or Simple Average Benchmark Rating (SABR) of 2.33 and above based on its most recent performance. There is no such criteria for private mandate portfolios.

However, the EPF reserves the right to disallow certain investments based on other quantitative or qualitative factors.

You can invest your entire Available Investment Amount. After clicking on the Investment tab on the i-Akaun (Member), your Available Investment Amount is shown under the BUY tab. For further information :

In order to enjoy the benefits offered by investing through the i-Akaun (Member), you may contribute up to RM60,000 per annum from your personal savings into your EPF accounts.

However, amounts from self-contributions may not be fully available for investments through MIS. This is because self-contributions are subject to the same conditions as compulsory EPF contributions. First, only 70% of self-contributions will be credited into your EPF Account 1, with the remaining 30% credited into your EPF Account 2. Secondly, any amount credited into your EPF Account 1 will be used to satisfy the Basic Savings first.

After clicking on the Investment tab on the i-Akaun (Member), your validity period is shown under the BUY tab. For further information:

Your eligible and Available Investment Amounts are applicable for 3 months only, beginning from any attempted MIS transactions after the end of the last validity period (if any).

For example, if you attempt a MIS transaction on 4 January 2019, the validity period will be from 4 January 2019 to 3 April 2019. You may make as many transactions as you wish within this validity period, subject to the Available Investment Amount. After 3 April 2019, if you attempt a MIS transaction on 1 May 2019, the updated validity period will be from 1 May 2019 to 31 July 2019

A FMI is a fund management institution approved by the EPF to offer eligible investments to EPF members. FMIs are typically unit trust management companies (UTMCs) or asset management companies (AMCs). FMIs are governed by the EPF’s Guidelines on EPF MIS

UTMCs pool funds from various investors and invest their funds based on a specific strategy or mandate. Investors own units that represent their proportional ownership of the unit trust fund’s net assets. Unit trust funds are more suitable for smaller investment amounts, as diversification is achieved by pooling funds from various investors

AMCs manage each investor’s portfolio based on a private mandate, taking into account the individual investor’s returns requirements, risk tolerance and constraints. Each investor fully owns his/her private mandate portfolio. Private mandate portfolios managed by AMCs are more suitable for larger investment amounts in order to achieve diversification.

Key SimilaritiesThe fee structures of both UTMCs and AMCs are similar. They charge an annual management fee, and also typically impose an initial sales charge. They typically invest in similar asset types, i.e. equity, bond, money market, mixed asset or property.

Funds offered by UTMCs can be distinguished by asset type (e.g. equity, bond, money market, mixed asset or property), geographical focus (e.g. ASEAN, Malaysia, global), Shariah or conventional status, risk/volatility indicators and performance metrics. On the i-Akaun (Member), you are able to filter and compare funds through the Investment tab using the Funds Selector function.

Private mandates offered by AMCs include non-discretionary, discretionary and semi-discretionary mandates. Discretionary mandates give the portfolio managers full investment control, while non-discretionary mandates give the clients full investment control. Semi-discretionary mandates give both portfolio managers and clients shared investment control.

Under MIS, only discretionary mandates are allowed for now. If you have previously established non-discretionary or semi-discretionary mandates, you are allowed to maintain those portfolios, but no additional funds can be injected. Portfolios managed by AMCs can invest directly into various asset types, or invest indirectly through approved unit trust funds.

An IUTA or Institutional UTS Adviser is a corporation registered with FIMM that is authorised to market and distribute various unit trust funds of FMIs. When investing through the i-Akaun (Member), approved unit trust funds of certain FMIs can only be transacted through IUTA platforms (this is because the relevant FMIs do not have their own platforms that are connected to the i-Akaun (Member).

FIMM or the Federation of Investment Managers Malaysia (formerly the Federation of Unit Trust Managers) is a self-regulatory organisation appointed by the Securities Commission Malaysia to regulate entities that market and distribute unit trust and private retirement schemes, including UTMCs.

The EPF releases control over investments through MIS, subject to any other conditions, under the following scenarios:

When the EPF releases control, you must deal directly with FMIs in relation to any investments previously made through MIS. If you redeem any investments, the proceeds cannot be deposited back into your EPF account(s), and must be deposited into your personal bank account. Kindly contact the relevant FMI for further clarification.

Generally, a unit trust fund is suitable for you if the fund’s risk and return profile matches your risk and return profile. Study the Fund Documents carefully to understand a fund’s risk and return profile. Your own risk and return profile depends mainly on your returns objective, risk tolerance and constraints. For example:

Your investment returns are generally impacted by, amongst others, your investment choices (in terms of asset class, sector, securities and geography), various risk factors, timing of investments, investment time horizon, and legal/tax considerations.

There are many risk factors that may impact your investment returns. For instance, equity price risk, liquidity risk, management risk, inflation risk, interest rate risk, etc. To read more, go to Learn More tab >> Unit Trust Investment >> General Risk of Investing.

MIS is a voluntary investment option for members. The EPF does not provide investment advice to individual members. You should fully understand the risks and expected returns before investing.

Any investment through MIS, including potential losses, is at the member’s own risk. Even in instances where your investments through MIS have performed well, the past is not representative of the future. The EPF’s declared dividends and the returns of investments through MIS are not equal comparisons.

The EPF has allowed investments through i-Akaun (Member) to empower members who are financially literate to take control of their investments. Through the i-Akaun (Member), you are able to analyse unit trust fund information, access anytime/anywhere, enjoy lower upfront fees of up to 0.5% (versus up to 3.0% previously), and view your fund/portfolio holdings on a consolidated basis. If you are aged 55 and above, you can still utilise the i-Akaun (Member) to invest conveniently with FMIs. However, EPF releases control over such investments, as they are withdrawals from your Akaun 55 and/or Akaun Emas.

If you are unable to determine the fund’s risk and return profile and your own risk and return profile, it is not advisable for you to invest through the i-Akaun (Member) self-service platform.

It is the paper gains/losses calculated based on changes in the NAV of the unit trust funds or private mandate portfolios. However, there is usually a time lag between your decision to sell and when your investments are actually sold; the NAV may change within this time interval.

Furthermore, the act of selling in itself may affect the NAV, especially if the investment is illiquid. Thus, the realised gains/losses (or sales proceeds) may differ from the unrealised gains/losses.

Yes. However, transactions submitted through i-Invest / i-Akaun during non-business days* will be processed on the next following business day. In general (unless specified differently in the respective fund’s prospectus), the cut-off time for the submission of unit trust transactions are as follow:

Money Market Funds – 10.00 a.m. (Please refer to the respective fund’s prospectus)

Equity/Mixed Asset/ Bond Funds – 4.00 p.m.

*Non-business days in refers to Saturday & Sunday, Public Holidays and Fund Holidays whenever applicable.

When EPF suspends an approved unit trust fund, you cannot buy or switch into the suspended fund. However, you may redeem from or switch out of the suspended fund. The EPF may suspend a fund for failing to meet performance requirements, e.g. for failing to meet a SACR or SABR of 2.33 and above.

When EPF freezes a fund, no transactions related to the frozen fund can be conducted. The EPF may freeze a fund pursuant to a FMI request prior to an income distribution or a unit split.

You can invest in unit trust funds through various ways. Below are step-by-step suggestions:

Option 1: You have a particular fund in mind

Option 2: You want to analyse different funds before investing

No. All investments with FMIs through MIS are not subject to any cooling-off period. Once an investment through MIS has been made, there is no grace period for any refund or cancellation.

Yes. Members are allowed to conduct unlimited transactions subject to the Available Investment Amount within the validity period.

Additional requirements and/or fees/charges may apply when members are completing the transaction on the FMI/IUTA platform.

No. Switching is only allowed between funds offered by the same FMI, subject to a switching fee (if any).

No. The ‘Total Investment’ represents the amount that is transferred out from your EPF Account 1 under the MIS. Therefore, the actual amount invested with FMIs will be less than the amount displayed, if an initial sales charge is imposed. Click here for more details.

It is an upfront charge imposed by FMIs for investing with them. The charge may differ across AMCs and unit trust funds offered by unit trust management companies (UTMC)s. However, the EPF has capped the initial sales charge at 0.5% for investments through the i-Akaun (Member), and 3.0% for investments through agents.

The charge will be deducted from the investment amount, without additional outflows from members. Please refer to the Fund Documents for additional details. Higher charges can significantly reduce your investment returns over the long term.

It is a fee imposed by FMIs and/or unit trust funds for the continuous management of your investments. The fee may differ across AMCs and unit trust funds offered by UTMCs. The fee is expressed in annual terms, but may be charged at more frequent intervals. The fee will be deducted from and reflected in the NAV of a unit trust fund, without additional outflows from members. Please refer to the Fund Documents for additional details. Higher fees can significantly reduce your investment returns over the long term.

It is a fee imposed by trustees (on UTMCs) or custodians (on AMCs) for the safeguarding of your assets with FMIs. The fee may differ across AMCs and unit trust funds offered by UTMCs. The fee is expressed in annual terms, but may be charged at more frequent intervals. The fee will be deducted from and reflected in the NAV of a unit trust fund, without additional outflows from members.

Please refer to the Fund Documents for additional details. Higher fees can significantly reduce your investment returns over the long term.

It is a fee imposed by FMIs for the continuous administration of your investments. The fee may differ across AMCs and unit trust funds offered by UTMCs. The fee is expressed in annual terms, but may be charged at more frequent intervals. The fee will be deducted from and reflected in the NAV of a unit trust fund, without additional outflows from members.

Please refer to the Fund Documents for additional details. Higher fees can significantly reduce your investment returns over the long term.

It is a backend fee imposed by FMIs for withdrawing your investments. The fee may differ across AMCs and unit trust funds offered by UTMCs. The fee will be deducted from the sale proceeds, without additional outflows from members

Please refer to the Fund Documents for additional details. Higher fees can significantly reduce your investment returns over the long term.

It is a fee imposed by FMIs for switching between unit trust funds offered by the same FMI. The fee may differ across unit trust funds. The fee will be deducted from the investment amount that is being switched, without additional outflows from members.

Please refer to the Fund Documents for additional details. Higher fees can significantly reduce your investment returns over the long term

It is calculated by taking the total assets of the fund minus the total liabilities of the fund:

NAV = Total assets - total liabilities

It is calculated by taking the NAV of the fund divided by the total number of units outstanding:

NAV per unit = NAV/(Total units outstanding)

The number of units purchased is the investment amount, net of any initial sales charge, divided by the NAV per unit. Please refer to the Fund Documents for additional details.

Example

Investment amount: RM10,000

Initial sales charge: 0.5%

NAV per unit on the purchase date: RM0.50

Investment amount net of initial sales charge

= Investment amount / (100% + Initial sales charge)

= RM10,000 / (100% + 0.5%)

= RM9,950.25

The sale proceeds is the number of units redeemed multiplied by NAV per unit, net of any redemption fees. Please refer to the Fund Documents for additional details.

Example

NAV per unit on the redemption date: RM0.50

Units redeemed: 19,900 units

Redemption fee: 1.0%

Investment value = NAV per unit x Units redeemed

= RM0.50 x 19,900

= RM9,950

The sale proceeds is the number of units redeemed multiplied by NAV per unit, net of any redemption fees. Please refer to the Fund Documents for additional details.

Example

NAV per unit on the redemption date: RM0.50

Units redeemed: 19,900 units

Redemption fee: 1.0%

Investment value = NAV per unit x Units redeemed

= RM0.50 x 19,900

= RM9,950

Redemption proceeds = Investment value x (100% - Redemption fee)

= RM9,950 / (100% + 1.0%)

= RM9,821.78

It is dividend or income earned by a unit trust fund that is distributed to unitholders.

For investments through MIS, income distribution will be reinvested and reflected as additional units in the relevant unit trust fund. For investments through MIS, income distribution through cash payout is not permitted.

The number of units reinvested is the total income distribution divided by the reinvestment price per unit. Please refer to the Fund Documents for additional details.

Example

Income distribution per unit: RM0.05

Units held: 10,000 units

Reinvestment price per unit = RM0.95

Total income distribution = Income distribution per unit x Units held

= RM0.05 x 10,000

= RM500

Units reinvested = Total income distribution / Reinvestment price per unit

= RM500 / RM0.95

= 526.32 units

You are entitled to income distribution if you are invested in a unit trust fund prior to its ex-dividend date and have not sold the investment prior to the ex-dividend date. For example, if the ex-dividend date is 7th March 2019, you must have invested in the unit trust fund on 6th March 2019 or earlier, and only sell the investments on 7th March 2019 or later

The ex-dividend dates may differ across unit trust funds offered by UTMCs. Please refer to the Fund Documents for additional details.

The number of units owned after switching is the investment amount to be switched, net of any switching fee, divided by the NAV per unit of the switching-in fund. Please refer to the Fund Documents for additional details.

Generally, a Shariah-compliant unit trust fund is a collective investment scheme that offers investors the opportunity to invest in a diversified portfolio of Shariah-compliant equity and fixed-income securities, as well as other Shariah-compliant money market instruments. The main objective of Shariah funds is to provide an alternative avenue for investors sensitive to Shariah requirements.

For example, Shariah funds will exclude those companies involved in activities, products or services related to conventional banking, insurance and financial services, gambling, alcoholic beverages and non-halal food products.

The main element that differentiates Shariah-compliant funds from other conventional funds is the appointment of a Shariah committee or adviser to determine the compliance of the fund with existing Shariah requirements.

No. As a Shariah EPF accountholder, you will not be able to invest in or switch into any conventional unit trust fund. However, your existing investments in conventional unit trust funds (made prior to converting your EPF account to a Shariah EPF account) will be maintained, until you redeem them.

No. Investments through MIS is neither return guaranteed nor capital guaranteed. You are advised to understand the risk and return profiles of approved unit trust funds before investing through MIS.

FMIs are licensed by the Securities Commission and hold a CMSL for fund management and/or CMSL for dealing in securities under the CMSA 2007. IUTAs are registered with FIMM, a self-regulatory organisation for the unit trust industry

To be registered with FIMM, IUTAs are licensed by the Securities Commission and hold a CMSL for dealing in securities under the CMSA 2007, or are registered persons under the CMSA 2007 dealing with interests in unit trust schemes as agents for investors. You can seek further clarification from the Securities Commission, FIMM and the relevant FMI or IUTA.

The EPF will take all necessary measures to ensure that your investments through MIS are safe even if the FMIs are suspended or terminated by the EPF. A suspended FMI must continue to manage your investments through MIS professionally and responsibly. You can switch your investments from a suspended FMI to a non-suspended FMI. However, a suspended FMI cannot receive additional investments through MIS.

Before a FMI is terminated, EPF will ensure that the FMI has liquidated members’ investments through MIS, and the proceeds are deposited safely back into their respective EPF accounts, according to directions issued by the EPF to the relevant FMI. At all relevant times, your investments are held by trustees or custodians, and kept separate from the FMI’s own assets.’

The EPF will take all necessary measures to ensure that your investments through MIS are safe even if the FMIs are not sustainable as a business entity. EPF will ensure that the FMI has liquidated members’ investments through MIS, and the proceeds are deposited safely back into their respective EPF accounts, according to directions issued by the EPF to the relevant FMI. At all relevant times, your investments are held by trustees or custodians, and kept separate from the FMI’s own assets.

The EPF will take all necessary measures to ensure that all transactions conducted through the i-Akaun (Member) are secure and safe. Before conducting any transaction, you will have to register their mobile numbers at an EPF branch or kiosk.

When a transaction is conducted through the i-Akaun (Member), Transaction Authorisation Code (TACs) will be sent by the EPF and relevant FMI to the member’s registered mobile number. You must enter the Transaction Authorisation Code (TACs) before a transaction can proceed

In addition, you will need to log into your i-Akaun (Member) and FMI/IUTA’s platform with your own passwords. All transactions through the i-Akaun (Member) are processed with strict security using the Secure Sockets Layer (SSL) protocol, the security standard used by the world's top financial institutions.

No. Members must register for the EPF’s i-Akaun (Member) to access its Investment tab.

When a member passes away, the EPF releases control over his/her investments through MIS. Therefore, the deceased’s heirs or administrators would have to deal directly with the relevant FMIs.

You may refer the dispute to the Securities Industry Dispute Resolution Center (SIDREC). SIDREC is an independent corporate body established for the settlement of monetary disputes between investors and SIDREC Members, who are CMSL holders or are registered by the Securities Commission Malaysia for the regulated activities of fund management, dealing in securities, dealing in derivatives and/or dealing in private retirement schemes. Members may visit https://www.sidrec.com.my for further details

The investment tab on the i-Akuan is an online, self-service function (i-Invest) to facilitate investments through MIS (Member Investment Scheme) in approved unit trust funds. To be eligible to invest via i-Akaun, members need to meet the basic savings requirement in the EPF account 1.

Yes, you will need to have an account with eUnittrust.com.my if you intend to place the EPF purchase order through our platform. For seamless transaction, it would be advisable if you create a free account opening with eUnittrust.com.my first.

However, if you do not have an eUnittrust.com.my account, system will redirect you to register a new investment account. Once you complete the account opening, you may continue the EPF transaction.

There are a list of EPF approved funds, you can click HERE to view the funds.

No, you no longer require to submit any physical form for EPF transaction via i-Invest in i-Akaun.

No, you can top up your existing fund without need to submit any EPF form

You can use our EPF Calculator to calculate your eligible investment amount.

You can use our EPF Calculator to calculate your eligible investment amount.

You can purchase unlimited funds; however, it is limited to one fund manager at a time only.

Unlimited. You can purchase EPF fund at any time provided you have sufficient balance in your EPF account 1. The eligible amount will valid for 3 months beginning from the attempted e-MIS transaction. EPF will refresh your new eligible investment amount after 3 months of your last EPF investment.

For example, if you attempt an e-MIS transaction on 3 January 2019, the validity period will count from 3 January 2019 to 2 April 2019. You can make unlimited transactions subject to your available balance in EPF account 1 within the validity period. After 3 months of your EPF order, EPF will refresh your new eligible amount and your new validity period for the new amount

The transaction cut off time for EPF i-Akaun is 4pm on every business day.

No. You can only switch your EPF fund within the same fund house

Yes, you can continue to use your EPF monies to invest EPF fund via i-Akaun

No, you can perform EPF transaction via website only

No, you are not able to purchase or switch your existing fund into conventional fund as Syariah EPF account only allows to invest in Syariah fund.

Incomplete account opening registration?Click here to resume